The Bank Called “Central Bank of India” — Not India’s Central Bank (And Why That Confuses Everyone)

If you hear the name Central Bank of India, your brain naturally assumes:

“Ah, that must be the bank that controls India’s money.”

But here’s the truth: Central Bank of India is not India’s central bank.

It never was.

It is one of India’s oldest commercial banks, and its story is not just about banking — it’s about nationalism, colonial economics, the Swadeshi movement, political power, and how India slowly built a financial system of its own.

And yes… its name has confused Indians for over a century.

Let’s unpack the real story — the one many people know only half of.

1) When Did Central Bank of India Start?

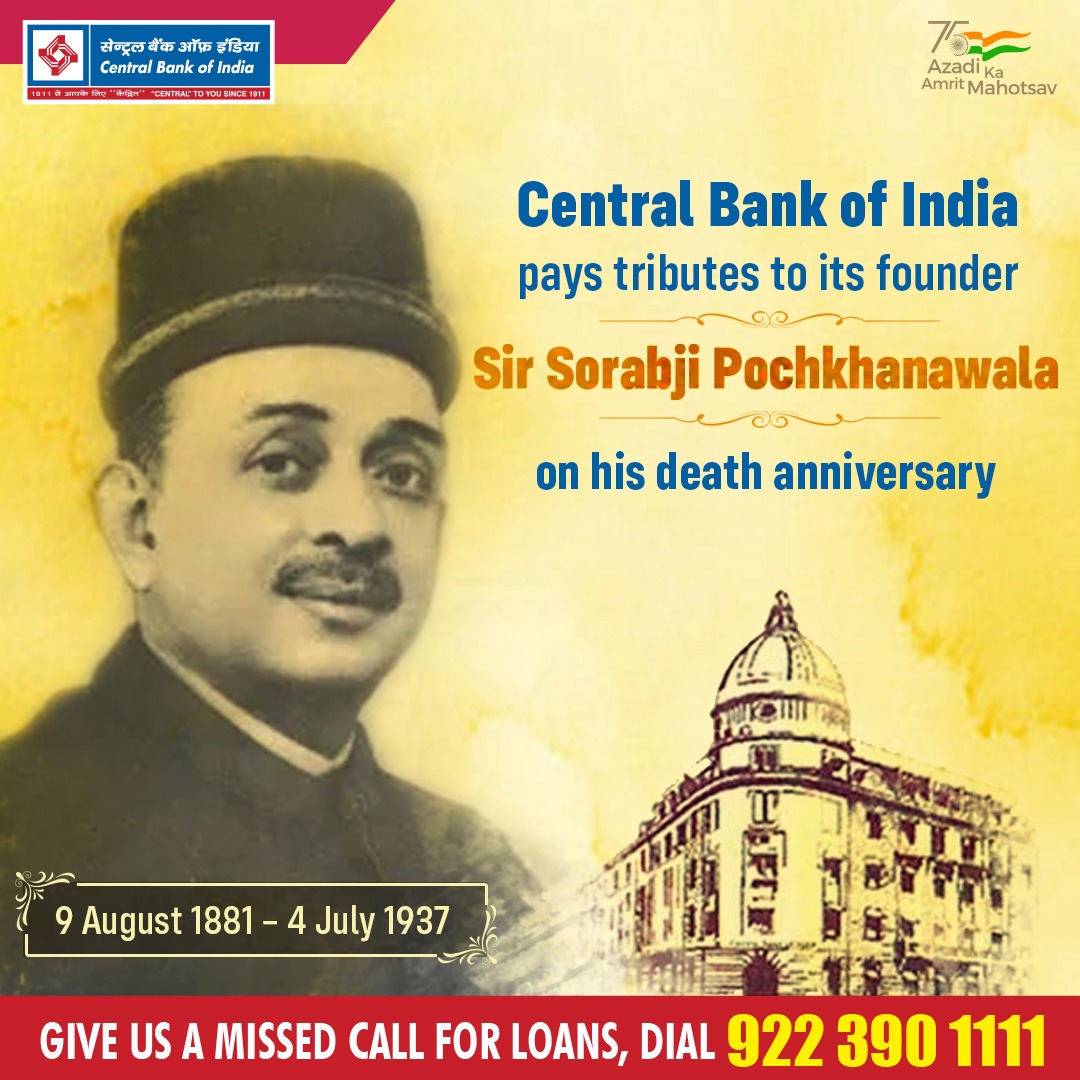

Central Bank of India was established on 21st December 1911.

This was a time when India was still under British rule, and banking power in India was largely controlled by British institutions and a few elite commercial networks.

India needed an Indian-owned banking identity.

That is exactly what Central Bank of India was created to become.

2) Who Started It?

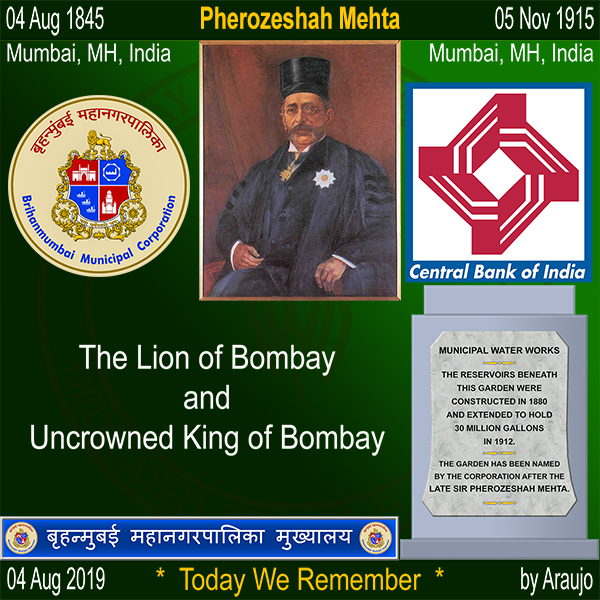

The founder was Sorabji Pochkhanawala, a visionary banker from the Parsi community.

But the bank’s identity became stronger because of one key public leader:

Sir Pherozeshah Mehta, a prominent Indian nationalist and leader, became the first Chairman.

This gave the bank credibility and trust among Indians who were beginning to push back against colonial control.

3) Why Was It Started? (The Real Purpose)

Central Bank of India was founded with a clear nationalist mission:

To build the first large Indian bank that was

- owned by Indians

- managed by Indians

- serving Indian business communities

- supporting Indian traders and industries

- functioning without British control

At that time, many Indian businesses were dependent on British banks and British financial systems. Those systems were designed mainly to support colonial trade, not Indian prosperity.

So Central Bank of India wasn’t just a business venture.

It was an economic freedom movement in the form of a bank.

4) The Early Performance — Was It Successful?

Yes. Surprisingly successful.

In its early years, Central Bank of India gained strong trust because Indians saw it as “their own bank.”

In the initial decades, the bank grew by focusing on:

- deposits from Indian communities

- credit to Indian traders

- support to small enterprises

- financing agricultural trade and local business activity

Unlike many banks that were mostly urban and elite-focused, Central Bank of India tried to expand across regions and communities.

One of the interesting historical points is that the bank expanded even beyond India into trade-linked regions like Rangoon (Burma), reflecting India’s commercial networks at that time.

So in the early stage, the bank performed well not because it had huge capital, but because it had something more powerful:

public trust and national pride.

5) The Peculiarity of Central Bank of India — The Name That Misled Generations

Here’s the most fascinating part:

Central Bank of India is a commercial bank, but its name sounds like a monetary authority.

This was not just a branding coincidence.

Back in the early 1900s, the term “Central” was used to represent importance and national scope.

But over time, it created confusion because many countries have “central banks” that control money supply, interest rates, currency printing, etc.

People still ask today:

“Is Central Bank of India under RBI or above RBI?”

The answer is simple:

RBI is the apex bank.

Central Bank of India is a regular bank under RBI regulations.

6) What Was India’s Banking Structure Like in Those Days?

Before the Reserve Bank of India came, India’s financial system was fragmented.

- Currency issuance was handled under colonial administration and selected institutions.

- Some large banks acted as semi-government financial agents.

- There was no single powerful independent monetary authority like modern economies have today.

Banks like Central Bank of India were growing as commercial institutions, but they were not controlling India’s currency or interest rates.

India needed something else — a true central bank.

7) Then Why Was the Reserve Bank of India Created?

The Reserve Bank of India (RBI) was created because India needed an institution to manage the entire monetary and financial stability system.

A central bank is not just a “big bank.”

It has responsibilities like:

- controlling money supply

- issuing currency

- regulating banks

- acting as lender of last resort

- managing government accounts

- managing foreign exchange reserves

- controlling inflation and interest rates

This is a completely different job compared to a commercial bank.

So RBI was created in 1935, and it began operations on 1st April 1935.

8) Did RBI “Replace” Central Bank of India?

Not exactly.

RBI did not replace Central Bank of India like a king replacing another king.

Instead, RBI was created to become the formal apex monetary authority, something that India lacked.

Central Bank of India continued functioning normally as a commercial bank — taking deposits, giving loans, expanding branches, serving customers.

But after RBI came into existence, the confusion became clearer:

India now had a real central bank.

And also had a commercial bank with “Central Bank” in its name.

So RBI became the government’s primary financial authority.

Central Bank of India remained important — but not as an apex institution.

9) The Big Turning Point: Nationalisation (1969)

The biggest shift in Central Bank of India’s journey came in 1969, when the Indian government nationalised 14 major banks.

Central Bank of India was one of them.

Nationalisation changed the purpose of Indian banks.

Instead of focusing only on profits and business-class customers, banks were pushed to serve national development goals, such as:

- rural branch expansion

- agricultural lending

- support to small-scale industries

- priority sector lending

- financial inclusion

This was a political and economic strategy.

India wanted banking to serve the masses.

10) What Happened After Nationalisation?

After becoming a public sector bank, Central Bank of India expanded heavily.

Its reach increased into:

- villages

- semi-urban towns

- underserved regions

- agriculture-heavy states

But this expansion also came with challenges.

Because public banks had political obligations, many loans were issued under social and political pressure. Over decades, this contributed to problems like:

- bad loans

- delayed recoveries

- weak profitability

- dependence on government recapitalisation

This wasn’t unique to Central Bank of India. It became a common issue across many public sector banks.

11) What Made Central Bank of India Unique Compared to Other Banks of That Era?

Several things stand out:

1. Nationalist Identity

It wasn’t born as a colonial tool. It was born as a Swadeshi statement.

2. Indian Ownership and Management

At a time when most major institutions were under British influence, this bank was fully Indian-led.

3. Strong Public Trust

Its early growth was powered by emotion, pride, and nationalism — not just marketing.

4. Expansion Outside India

The bank’s early overseas presence reflected India’s trading strength even under colonial rule.

5. Its Name

The name itself became both its advantage and its lifelong confusion.

12) The Harsh Truth: Why Central Bank of India Lost “Prestige” Over Time

Let’s be honest.

Central Bank of India is historically important, but in today’s banking market, prestige is driven by:

- technology

- speed

- customer experience

- digital banking

- aggressive expansion

- strong financial performance

- modern corporate banking strength

Private banks like HDFC, ICICI, Axis, and Kotak redefined what “good banking” looks like in India.

Public banks, including Central Bank of India, struggled with:

- slower modernization

- weaker digital experience (historically)

- bureaucratic culture

- rising NPAs during certain economic cycles

- limited innovation compared to private competitors

That doesn’t mean the bank became irrelevant.

But it does mean it stopped being seen as “elite.”

13) Current Status: Where Does Central Bank of India Stand Today?

Today, Central Bank of India is still a major public sector bank with:

- a large branch network

- strong rural and semi-urban presence

- government trust

- millions of customers

- a long legacy

It continues to function as a full-service bank offering:

- savings and current accounts

- fixed deposits

- retail loans

- home loans and personal loans

- MSME finance

- agriculture lending

- digital banking platforms

But here’s the reality:

Central Bank of India today does not command the same class or premium image as top private banks.

Yet it holds a different kind of power:

It holds stability.

It holds reach.

It holds legacy.

In India, legacy is not a small thing.

14) Does Central Bank of India Still Hold the Same “Class”?

If “class” means luxury and premium customer experience like modern private banks, then no.

But if “class” means:

- trust

- government-backed stability

- rural inclusion

- national presence

- long-standing credibility

Then yes — it holds a different kind of class.

It is the kind of bank your grandfather trusted without even asking interest rates.

And that kind of trust is rare.

15) The Most Thought-Provoking Part: The Name Itself Is a Lesson

Central Bank of India’s name is a metaphor for India.

India has always carried names, symbols, and legacies that are bigger than their actual function today.

The bank is called “Central,” but it is not central in authority.

Yet it is central in history.

The RBI is the real apex bank, but it came later.

So the real lesson is this:

Institutions don’t stay powerful forever.

Power shifts to whoever adapts.

And banking is not about who started first.

Banking is about who evolves faster.

16) Final Thought: Why Central Bank of India Still Matters in Modern India

In a country obsessed with startups, fintech, UPI speed, and app-based banking, we often forget something:

India did not build its economy through apps.

India built its economy through institutions.

Central Bank of India is one such institution.

It may not dominate headlines like private banks, and it may not look glamorous in urban India, but it still carries a legacy that cannot be erased:

It was built when Indians were still fighting for economic identity.

It was built when banking was a tool of colonial control.

It was built when trust was more valuable than technology.

And it still stands today.

Not as a ruler of India’s banking system.

But as a survivor of India’s financial evolution.

That is not just history.

That is resilience.

In One Line

Central Bank of India is not India’s central bank — but it is one of India’s most historically important banks, born out of nationalism, reshaped by nationalisation, and still standing in a market now ruled by speed-driven private banking giants.

Comments

Hi, I’m Nishanth Muraleedharan (also known as Nishani)—an IT engineer turned internet entrepreneur with 25+ years in the textile industry. As the Founder & CEO of "DMZ International Imports & Exports" and President & Chairperson of the "Save Handloom Foundation", I’m committed to reviving India’s handloom heritage by empowering artisans through sustainable practices and advanced technologies like Blockchain, AI, AR & VR. I write what I love to read—thought-provoking, purposeful, and rooted in impact. nishani.in is not just a blog — it's a mark, a sign, a symbol, an impression of the naked truth. Like what you read? Buy me a chai and keep the ideas brewing. ☕💭 For advertising on any of our platforms, WhatsApp me on : +91-91-0950-0950 or email me @ support@dmzinternational.com